News

•

05/05/2026

With the proliferation of AI content, the skills to discern reality from imitation have become increasingly important. One of the easiest tells for AI generated content is noticing a sixth finger on a person’s hand. AI technology is impressive and we see the appeal of near-instant creation of humorous videos, but when it comes to your investments, you probably don’t want a sixth finger.

The Sixth Finger

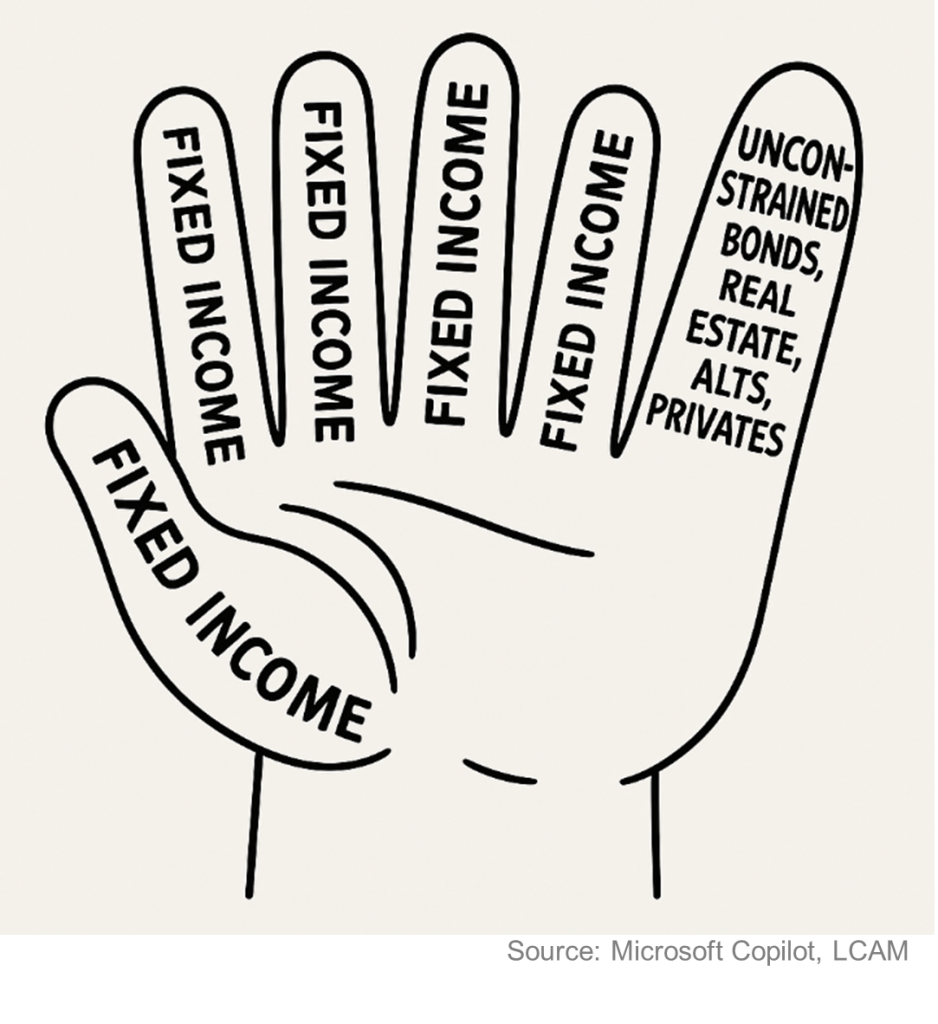

The low rates period from the end of the 2008 financial crisis until 2022, incentivized investors to find ever more creative replacements for traditional fixed income. These alternatives took many forms, including: unconstrained bond strategies, real estate, ‘carry trades’, global currencies, equity dividend strategies, covered call strategies and various alternative and private strategies. In some cases, these strategies were designed to utilize fixed income instruments, but with reduced market exposure, while in other cases they were designed as income replacement. Typically, there is some trade-off for these strategies versus true fixed income, possibly including lock-ups, leverage or alternative risk factors, which perform differently than fixed income when fixed income performance is needed.

Five Fingers is Just Fine

In 2025, the broad fixed income benchmark returned over 7%. Though fixed income returns are often discussed in the context of rate changes, 10-year Treasury yields only declined by about 40 basis points, while the bulk of the returns was driven by high quality income generation. Even with major geopolitical events in the first quarter of 2026, bond income offset the mild increase in yields, leading to an effectively flat returns for the quater. With yields on the Bloomberg Aggregate above 4.5% at the end of the first quarter, the potential for another predictable, solid year remains strong despite broader uncertainties.

Not Tying Your Hands

That traditional fixed income can deliver attractive returns, without the lockups and leverage, should attract attention, particularly as the replacements have had mixed results. Importantly, there are many opportunities to enhance returns without long lock-ups or leverage.

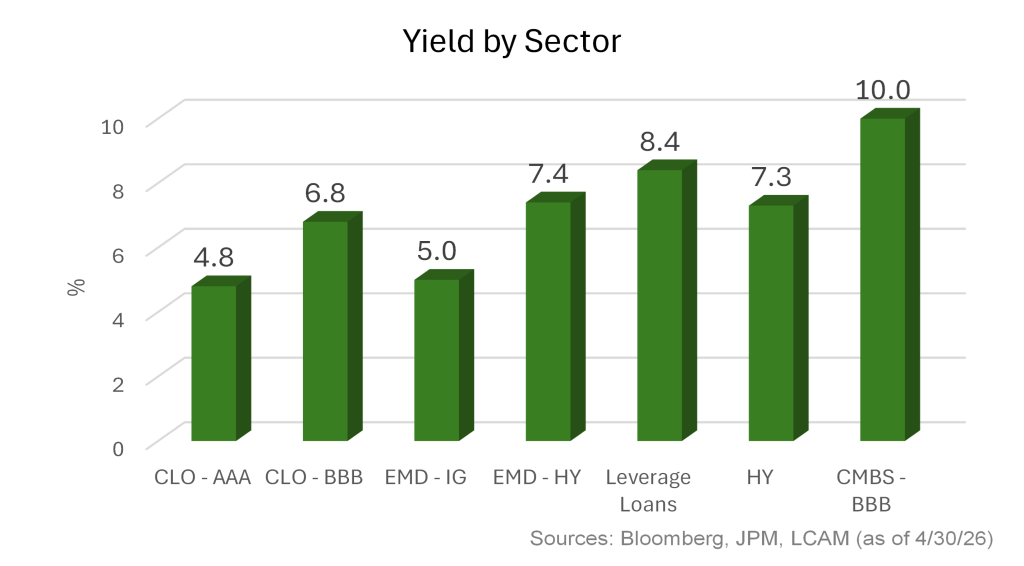

As the market reached for fixed income proxies, market segments that were once considered unconventional or niche have become increasingly mainstream. As we have noted in the past, high yield was once a relatively obscure segment called ‘junk’, before becoming a fixed income mainstay with over $1.5 trillion of outstanding bonds. Similarly, the increased adoption of segments like broadly syndicated loans, CLOs and securitized credit have improved liquidity and reduced trading costs, allowing borrowers to select which instrument to issue based on which is most advantageous for them to raise capital.

Building with Real Hands

Interestingly, the mainstreaming of these higher yielding assets helps establish a broader continuum for fixed income investors. Certainly, these assets offer different risk, return and liquidity profiles than Treasuries, Agency Mortgages and Investment Grade Credit, the most standard broad fixed income market components. While the trade-off of higher volatility for higher yield is real, these instruments also create the ability to construct portfolios with yields approaching more alternative vehicles without lengthy lock-up periods.

Conclusions: A Keen Eye is Needed as Sixth Fingers Proliferate

The opportunity set for fixed income has never been broader or deeper. The most standard broad markets, after returning 7% last year, continue to offer compelling yields in addition to liquidity and the diversifying effects sought in a broad asset allocation. The increased adoption of higher yielding segments allows more diversified approaches to income generation without leaving the liquid public markets. Today’s markets require a keen eye and steady hand and, as always, remember to look out for that sixth finger.

|

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This publication is prepared for general information only. This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested. Investments cannot be made in an index. Past performance is not necessarily a guide to future performance. Loop Capital Asset Management – TCH, LLC is a registered investment adviser and a wholly owned subsidiary of Loop Capital Asset Management, which is a subsidiary of Loop Capital LLC. Loop Capital is the brand name for various affiliated entities of Loop Capital LLC that provide investment banking, and investment management services. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. Loop Capital is a trademark of Loop Capital Holdings LLC. Loop Capital Asset Management LLC, and Loop Capital Markets LLC are affiliated companies. Investment products are: Not A Deposit | Not FDIC Insured | No Bank Guarantee | May Lose Value |